The Real Estate Resurgence:

Blueprint For Building Billions Brick By Brick

Authors: Kasak Agarwal, Suhana Purohit, Prayag Patnaik, Saman Quasim & Satyam Agarwalla

Overview

The Real Estate sector is a multibillion-dollar industry that currently contributes 7 percent to India’s GDP. It is one of the most vital sectors of the Indian economy, comprising four sub-sectors: housing, retail, hospitality, and commercial real estate establishments. This sector is the second-highest employment generator after agriculture. It is expected to account for 10-13 percent of India’s GDP by 2025 (IBEF, 2021), with the market size anticipated to reach USD 1 trillion by 2030.

According to a report by Colliers India, there are 17 emerging real estate hotspots in India. These include Amritsar, Ayodhya, Jaipur, Kanpur, Lucknow, and Varanasi in the North; Patna and Puri in the East; Dwarka, Nagpur, Shirdi, and Surat in the West; and Coimbatore, Kochi, Tirupati, and Visakhapatnam in the South, as well as Indore. Furthermore, with a rising economy and massive infrastructure development projects coming up across India, the real estate industry is anticipated to display robust growth in the coming years.

Industry Trends

The initial decades of the real estate industry were marked by slow aggregate growth. The absence of swift loan schemes, lack of foreign investment, bureaucratic red-tapism and regulatory hurdles delaying approvals were key problems of the industry. The economic liberalization of 1991 led to increased interest of foreign investors in the Indian Real Estate industry due to the massive growth potential of Indian markets.

The financial crisis of 2008, although originating in the American markets, had widespread repercussions for Indian markets, particularly for India’s Real Estate industry. During this time, property prices surged up to 60% in cities like Mumbai and Bangalore, which led to a drastic decline in property sales.

Following the crisis, the industry embarked on a slow recovery from an unpromising state. The aftereffects of the 2008 financial crisis impacted the industry until the end of 2013, with large companies filing for bankruptcy and people losing their homes. In 2014, the Indian government began introducing initiatives like the Pradhan Mantri Awas Yojana to boost the real estate ecosystem. Once the market stabilized, Foreign Direct Investment (FDI) grew gradually, and the industry saw steady growth of 10-20% annually, with rising sales each year.

With the Indian economy growing at a rapid rate and on the path to becoming a global economic power, the real estate sector is now contributing 7.3% to the GDP, up from less than 3% in 2010. Recently, the green building economy, driven by eco-friendly and sustainable construction approaches, has also taken a tangible shape in India. Over 7000 IGBC (Indian Green Building Council) certified green projects have occupied an estimated 1370 million sq ft land as of 2024.

Key Stakeholders, Market Share Dynamics & Leading Players

in India’s Real Estate Industry

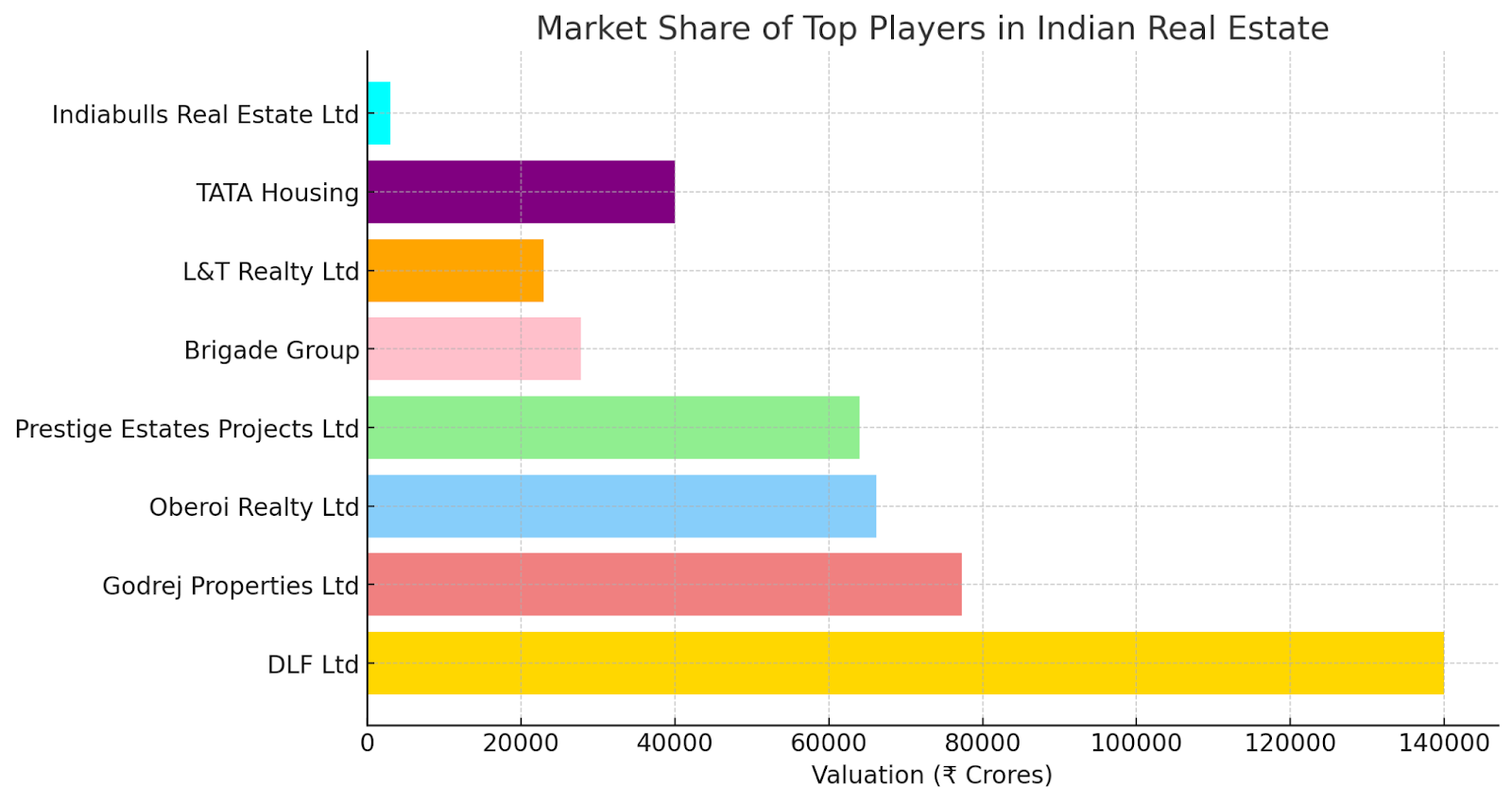

With the rapid economic growth across the country, the real estate industry is witnessing a transformation within itself which is manifested by major RE companies that are spread across the horizon of residential, commercial, retail, and hospitality spaces. A new sub-sector has emerged in recent years as a result of government policies, that is the declaration of an area as a Special Economic Zone (SEZ). These sub sectors are hauled by few major companies. Some of these companies include seasoned players like DLF Ltd. (Est.1946) with key projects like DLF City in Gurgaon and the list also includes young players like Equinox India Development Ltd. (formerly IndiaBulls Ltd., Est. 2005) and L&T Realty Ltd. (Est.2011).

The following graph shows market valuation of the key stakeholders:

Government Initiatives for Promoting the Real Estate Industry

To address issues related to transparency, accountability, and project clearance delays, the Real Estate (Regulation and Development) Act, 2016 established a Real Estate Regulatory Authority to regulate real estate transactions and protect buyers from malpractices. The Indian Government has allowed 100% Foreign Direct Investment (FDI) in real estate development projects.

The Smart Cities Mission, under the Ministry of Urban Development, aims to develop 100 smart cities. Additionally, the Pradhan Mantri Awas Yojana (PMAY) aims to sanction the construction of 3.8 crore houses across the nation. PMAY addresses housing shortages for lower and lower-middle-income groups, with the Budget 2023-24 allocating Rs. 79,000 crores to the program, a 66% increase from the previous budget. Furthermore, the Union Cabinet has approved an Alternative Investment Fund (AIF) to rejuvenate 1,600 halted housing projects in major Indian cities. The 2024 budget also reduced the long-term capital gains tax on real estate transactions from 20% to 12.5%.

Real Estate Investment Trusts (REITs)

Real Estate Investment Trusts in India were brought out, in 2007, by SEBI as a vehicle to channel small investors’ funds for investment into real estate, allowing investors to buy and sell shares in a portfolio of properties on the open market instead of directly in real estate. Today, there are five registered REITs, out of which four have successfully come out to the public markets, with a combined market capitalization of over Rs. 80,000 crores. Consistent returns, portfolio diversification, and increased liquidity characterize REITs, making them popular investment choices for the investors today. Entry of REITs has encouraged institutional investment in real estate. Institutional investors, encompassing pension funds and insurance companies, are more eager to invest in regulated vehicles such as REITs since they bring about diversification and minimize the risk attached to investments. This influx of funds finances large commercial projects and fuels growth in the real estate sector.

Furthermore, REITs encouraged the development of infrastructure and commercial properties because they pursued income-producing assets. Such developments have catalyzed better urban development and increased employment opportunities, hence enhancing the economy’s growth.

What Is Ahead of Us?

The prowess of the Real Estate Industry can be demonstrated in its ability to create 31 million jobs from 2013 to 2023 with the total workforce employed rising from 40 million to 71 million Indians in one decade. Employing more than 18% Indian workforce and supporting around 250 ancillary industries, the industry is a force too big to fail. Exponential growth is expected to push the industry ahead upto 2047 while investments in the sector are expected to touch USD 59.7 billion by 2047. Lastly, the fact that the green building industry of India is also expected to rise to USD 39 billion by 2025, is what makes us feel that the real estate industry is here to both boom in profits and contribute towards sustainability.

𝑫𝒊𝒔𝒄𝒍𝒂𝒊𝒎𝒆𝒓: 𝑻𝒉𝒆 𝒃𝒍𝒐𝒈 𝒓𝒆𝒇𝒍𝒆𝒄𝒕𝒔 𝒕𝒉𝒆 𝒗𝒊𝒆𝒘𝒔 𝒐𝒇 𝒕𝒉𝒆 𝒂𝒏𝒂𝒍𝒚𝒔𝒕 𝒂𝒏𝒅 𝒊𝒔 𝒊𝒏𝒅𝒆𝒑𝒆𝒏𝒅𝒆𝒏𝒕 𝒐𝒇 𝒕𝒉𝒆 𝒗𝒊𝒆𝒘𝒔 𝒐𝒇 𝑺𝒕. 𝑿𝒂𝒗𝒊𝒆𝒓’𝒔 𝑪𝒐𝒍𝒍𝒆𝒈𝒆 (𝑨𝒖𝒕𝒐𝒏𝒐𝒎𝒐𝒖𝒔), 𝑲𝒐𝒍𝒌𝒂𝒕𝒂